Streamlining Subrogation: A Comprehensive Insurance Claims Subrogation Workflow Template

Published: 06/04/2026 Updated: 06/05/2026

Table of Contents

- Introduction to Efficient Subrogation Management

- Phase 1: Initial Identification and Data Gathering

- Phase 2: Assessing Liability and Recoverable Amounts

- Phase 3: Case Creation and Investigative Setup

- Phase 4: Evidence Verification and Documentation

- Phase 5: Third-Party Communication and Demand Execution

- Phase 6: Monitoring Deadlines and Managing Negotiations

- Phase 7: Settlement Analysis and Loss Variance Calculation

- Phase 8: Finalizing Case Outcomes and Claim Updates

- Phase 9: Reporting, Auditing, and Archive Management

- Resources & Links

TLDR: This guide introduces a comprehensive subrogation workflow template designed to automate and standardize the recovery process. Learn how to transition from initial claim identification to final settlement and reporting, ensuring every step-from evidence verification to demand letter follow-ups-is executed efficiently to maximize cost recovery and minimize manual errors.

Introduction to Efficient Subrogation Management

Subrogation is a critical component of the insurance lifecycle, representing the process by which an insurer seeks to recover claim costs from the responsible third party. When managed effectively, it transforms a cost center into a powerful recovery engine, directly impacting an organization's loss ratio and overall profitability. However, the complexity of subrogation lies in its multifaceted nature; it requires meticulous attention to detail, rigorous evidence verification, and seamless coordination between various stakeholders, including third-party insurers and claimants.

The primary challenge in subrogation is not just identifying potential recovery opportunities, but managing the intricate web of tasks required to finalize them. Without a standardized, systematic workflow, claims can easily stall due to missed deadlines, lost documentation, or inadequate investigation. An efficient subrogation management strategy relies on a structured sequence of actions-ranging from the initial identification of third-party liability to the final settlement approval and reporting. By implementing a disciplined workflow, insurers can ensure that no recoverable amount is left on the table, reducing leakage and ensuring that the recovery process is both transparent and highly scalable.

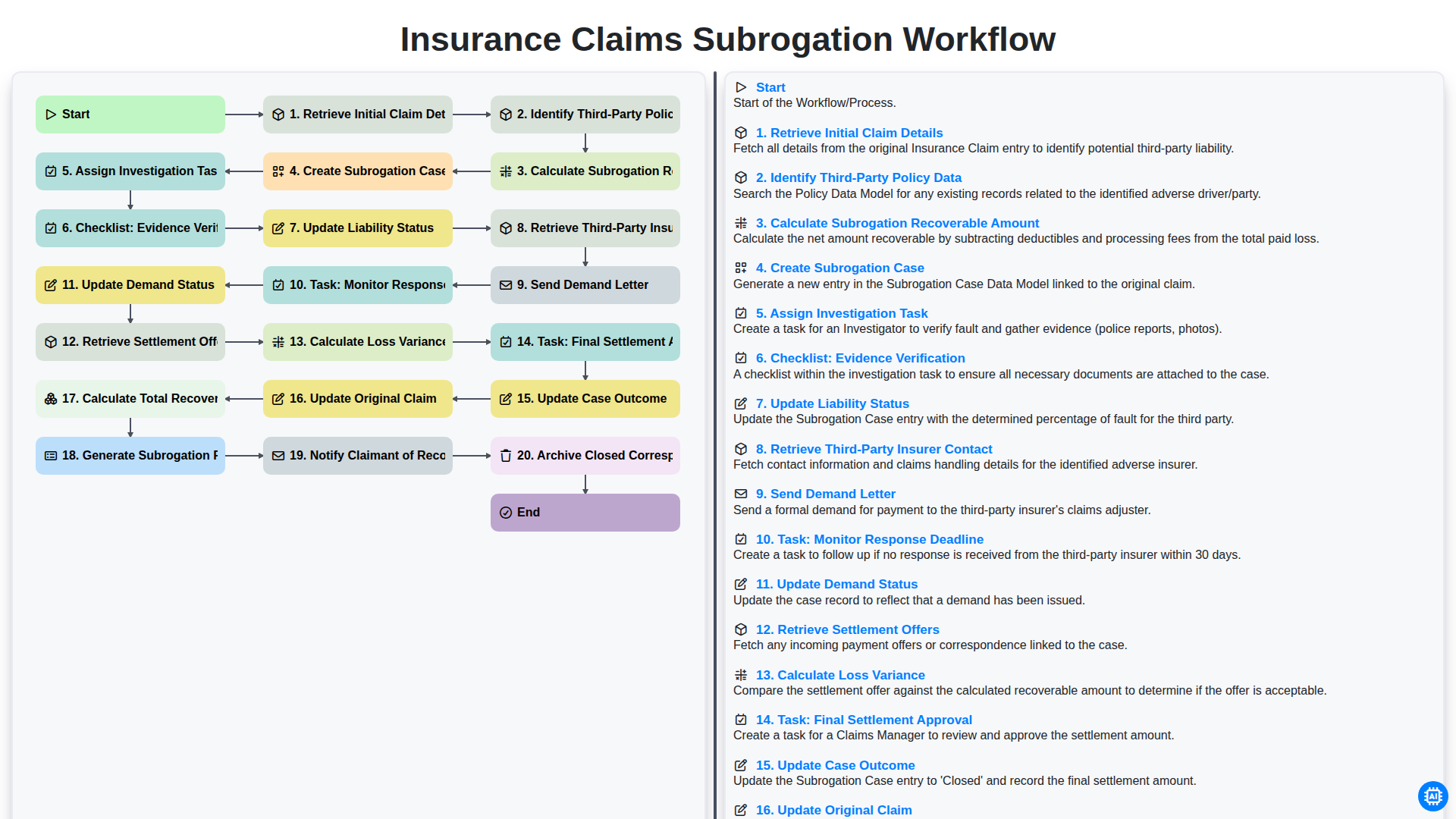

Phase 1: Initial Identification and Data Gathering

The subrogation process begins long before a formal demand is sent; it starts the moment a claim is filed. The primary goal of this initial phase is to establish a clear foundation of facts to determine if a third party is legally responsible for the loss.

The workflow begins by retrieving initial claim details from the original loss report. This involves a deep dive into the circumstances of the incident to understand what happened, when it happened, and who was involved. Once the core details are established, the next critical step is to identify third-party policy data. By pinpointing the other involved party's insurance carrier and policy information, adjusters can determine the scope of potential recovery.

With the groundwork laid, the focus shifts to financial feasibility. The team must calculate the subrogation recoverable amount, ensuring that the potential for recovery outweighs the operational costs of pursuing the claim. If the math supports the pursuit, the system moves to create a subrogation case, formally separating the recovery effort from the original loss claim. Finally, to ensure no detail is overlooked, an assign investigation task is triggered, prompting a specialist to begin a detailed review of the incident's liability.

Phase 2: Assessing Liability and Recoverable Amounts

Once the initial claim details have been retrieved and the third-party policy data is identified, the workflow moves into the critical analytical stage: assessing liability and determining the potential for recovery. This phase is the backbone of a successful subrogation strategy, as it determines whether the expense of pursuing a claim is justified by the potential payout.

The process begins with the precise calculation of the subrogation recoverable amount. This involves a meticulous audit of all payments made toward the loss to ensure that only valid, reimbursable expenses are included. Once this figure is established, the system initiates the formal creation of the subrogation case, effectively transitioning the file from a standard claim to a recovery-focused investigation.

With the case established, the focus shifts to active investigation. An investigation task is assigned to a specialist, who must work through a rigorous evidence verification checklist. This step is crucial for ensuring that all documentation-such as police reports, photos, and witness statements-supports the claim against the third party. As the evidence is reviewed, the specialist will update the liability status, providing a real-time indication of the strength of the subrogation opportunity. This rigorous assessment ensures that resources are focused only on high-probability recovery cases.

Phase 3: Case Creation and Investigative Setup

Once the initial assessment confirms a potential for recovery, the workflow transitions from data gathering to active case management. This phase is critical, as it involves transforming raw claim data into an actionable legal and investigative framework.

The process begins with Calculating the Subrogation Recoverable Amount, a vital step to ensure that the potential recovery justifies the administrative costs of pursuing the third party. Once the financial viability is confirmed, the system proceeds to Create a Subrogation Case, officially separating the recovery efforts from the initial loss claim.

With the case established, the focus shifts to active investigation. The next step is to Assign an Investigation Task to a dedicated subrogation specialist or adjuster. To ensure no critical detail is overlooked during this period, a rigorous Checklist: Evidence Verification is implemented. This ensures that all necessary documentation-such as police reports, photos, and witness statements-is authenticated and ready for use. Finally, the specialist must Update Liability Status, providing a clear, real-time indication of whether the third party's liability is established, disputed, or still under review.

Phase 4: Evidence Verification and Documentation

Once the subrogation case has been officially created and the investigation task assigned, the focus shifts to the most critical stage of the process: building a bulletproof evidentiary foundation. This phase is centered around a rigorous Checklist: Evidence Verification, where investigators meticulously audit all available documentation to ensure the claim is defensible.

The primary goal here is to validate the strength of the recovery potential by confirming that all supporting documents-such as police reports, eyewitness statements, photos of the scene, and damage assessments-are accurate, complete, and legally admissible. During this stage, the investigator must also Update Liability Status. This involves a deep dive into the facts to determine if the third party's negligence is clearly established or if there are any contributory factors that might diminish the recoverable amount. A thorough verification process at this stage prevents the pursuit of meritless claims and ensures that when you eventually move to the demand stage, your position is backed by indisputable proof.

Phase 5: Third-Party Communication and Demand Execution

Once the investigation has established a clear path toward recovery, the workflow shifts from internal assessment to active external engagement. This phase is critical, as it involves direct interaction with the third-party insurer to formalize the demand for reimbursement.

The process begins by retrieving third-party insurer contact information to ensure all legal notices are directed to the correct claims adjuster. With the necessary details in hand, the next decisive step is to send the demand letter. This formal document outlines the facts of the loss, the evidence collected during the investigation, and the specific amount being sought for reimbursement.

Because timely follow-up is essential to preventing claims from stagnating, a dedicated task to monitor response deadlines must be implemented. This ensures that no demand sits unaddressed and that the subrogation specialist can pivot to next steps if the third-party carrier fails to respond within the statutory or reasonable timeframe. As communications progress, you must consistently update the demand status within your management system to maintain a real-time view of all pending recoveries.

Phase 6: Monitoring Deadlines and Managing Negotiations

Once the demand letter has been dispatched, the workflow shifts from proactive pursuit to diligent oversight. This stage is critical, as the success of subrogation often depends on rigorous follow-up and precise administrative tracking.

The process begins with the essential Task: Monitor Response Deadline. Subrogation recovery is time-sensitive; failing to follow up on a pending demand can lead to missed recovery windows or statutory limitations. As the deadline approaches, the adjuster must Update Demand Status to ensure the file reflects the current stage of negotiation, providing transparency to all stakeholders involved.

When communication from the third-party insurer is received, the focus moves to evaluation. The adjuster must Retrieve Settlement Offers and begin the analytical process of comparing the offer against the established loss. This involves the critical step to Calculate Loss Variance, identifying any discrepancy between the initial recoverable amount and the proposed settlement.

The final gatekeeper in this phase is the Task: Final Settlement Approval. Before any funds are finalized, the discrepancy must be reviewed to ensure the settlement is in the best interest of the company. Once approval is secured, the workflow moves toward closure, ensuring that the negotiation is documented and the path is cleared for the final distribution of funds.

Phase 7: Settlement Analysis and Loss Variance Calculation

Once a settlement offer is received from the third-party insurer, the workflow enters a critical stage of financial reconciliation. The primary objective during this phase is to Retrieve Settlement Offers and perform a rigorous Calculate Loss Variance procedure. This involves comparing the incoming offer against the total indemnity and expense payments made on the original claim to identify any discrepancies or gaps in recovery.

It is essential to determine if the offer covers the full extent of the loss or if there is an unrecoverable deficit. This calculation ensures that the subrogation team can pinpoint exactly where leakage is occurring within the claims process. By analyzing this variance, adjusters can decide whether to accept the current offer or escalate the matter for further negotiation, ensuring that the final recovery remains as close to the total paid loss as possible.

Phase 8: Finalizing Case Outcomes and Claim Updates

Once the settlement negotiations conclude, the workflow transitions into the critical finalization phase. The process begins with the formal Task: Final Settlement Approval, ensuring that the negotiated amount aligns with the company's recovery objectives. Following approval, the system must Update Case Outcome to reflect whether the subrogation was successful, partially successful, or denied.

Precision is vital during this stage; the Update Original Claim step ensures that the primary claim file is adjusted to reflect the recovered funds, maintaining an accurate ledger. To maintain high-level oversight, the workflow triggers a calculation to Calculate Total Recovered Monthly, allowing for real-time tracking of recovery performance against targets. This data feeds directly into the final administrative step: Generate Subrogation Recovery Report, providing stakeholders with actionable insights into subrogation efficiency.

Finally, to ensure transparency and compliance, the system will Notify Claimant of Recovery regarding any applicable reimbursements and Archive Closed Correspondence, ensuring a complete and organized audit trail for every resolved case.

Phase 9: Reporting, Auditing, and Archive Management

The final phase of the subrogation lifecycle focuses on long-term data integrity, financial oversight, and administrative closure. Once the settlement is finalized, the workflow moves into a critical period of auditing and reporting to ensure all recovered funds are accurately accounted for and documented.

This stage begins with the calculation of the total recovered monthly amount, providing a high-level view of the recovery performance for the period. To maintain transparency and operational insight, a Subrogation Recovery Report is generated, allowing stakeholders to analyze trends, success rates, and loss mitigation efficiency.

Beyond high-level reporting, the workflow ensures all individual stakeholders are informed by notifying the claimant of the recovery, ensuring transparency regarding the final resolution of their claim. Finally, to maintain a clean and organized digital workspace, the process concludes with the archiving of all closed correspondence. This ensures that every piece of evidence, communication, and legal documentation is preserved for future audit requirements or potential disputes, effectively closing the loop on the subrogation journey.

Resources & Links

- Insurance Information Institute (III): A primary source for industry statistics, trends, and educational resources regarding insurance subrogation processes and legal standards.

- Claims Association: Professional resources and industry best practices for claims professionals focusing on litigation and recovery workflows.

- Legal Information Institute (LII): Access to legal definitions and frameworks regarding liability, negligence, and third-party recovery regulations.

- Claims Management Software Guide: Insights into how automation and digital workflows can streamline the identification and demand phases of subrogation.

- Financial Reporting Standards for Insurance: Resources for calculating loss variance, recovering amounts, and managing monthly subrogation recovery reporting.

- Evidence and Documentation Standards: Best practices for maintaining a checklist for evidence verification and maintaining an audit trail for closed correspondence.

Found this Article helpful?

Insurance Management Solution Demo

Managing policies, claims, and compliance in the insurance industry is complex. ChecklistGuro's Work OS platform streamlines your operations, from underwriting and renewals to claims processing and reporting. Improve efficiency, reduce errors, and enhance customer satisfaction. Discover how ChecklistGuro can transform your insurance business!

Related Articles

Streamline Claims: Your Insurance Claims Support Process Checklist Template

Your Insurance Policy Review Checklist: A Step-by-Step Guide

Your Property Insurance Review Checklist: A Step-by-Step Guide

Your Title Search & Insurance Checklist Template

Simplify Insurance Verification: Your Free Dental Checklist Template

Crop Insurance Policy Review Checklist: A Farmer's Guide

The Ultimate Vehicle Registration & Insurance Validation Checklist

Mastering the Policyholder Journey: Your Insurance Experience Survey Checklist

We can do it Together

Need help with

Checklists?

Have a question? We're here to help. Please submit your inquiry, and we'll respond promptly.