A Step-by-Step Guide to the Annual Budgeting and Cost Control Process

Published: 06/18/2026 Updated: 06/19/2026

Table of Contents

- Introduction to Annual Budgeting and Cost Control

- Phase 1: Data Collection and Aggregation

- Retrieving Departmental Budgets and Actual Expenses

- Phase 2: Quantitative Analysis and Variance Calculation

- Calculating Total Planned Budget and Actual Spend

- Measuring Performance: Budget Variance and Percentage Analysis

- Phase 3: Review and Audit Workflow

- Departmental Reviews and Finance Auditing

- Phase 4: Finalizing Adjustments and Status Updates

- Managing Budget Adjustments and Approval Notifications

- Proactive Monitoring: Handling Over-Budget Scenarios

- Phase 5: Reporting and Process Cleanup

- Generating the Annual Budget Summary Report

- Finalizing the Cycle: Cleaning Up Draft Budgets

- Resources & Links

TLDR: Streamline your financial oversight with this comprehensive guide to the Annual Budgeting and Cost Control workflow. Learn how to automate everything from budget retrieval and variance analysis to automated alerts for over-budget scenarios, ensuring precise financial auditing and seamless budget adjustments for your entire organization.

Introduction to Annual Budgeting and Cost Control

Managing a company's financial health requires more than just tracking cash flow; it demands a structured, proactive approach to resource allocation and expenditure monitoring. The Annual Budgeting and Cost Control Process serves as the strategic blueprint for an organization, providing a roadmap for financial stability and long-term growth.

At its core, this process is about more than just setting numbers in a spreadsheet. It is a continuous cycle of planning, monitoring, and adjusting that ensures every department remains aligned with the company's overarching fiscal goals. By implementing a standardized workflow, organizations can move away from reactive firefighting and toward a proactive culture of accountability. Through meticulous variance analysis and disciplined oversight, businesses can identify potential financial leaks before they become crises, optimize departmental spending, and ensure that capital is deployed where it can drive the most significant impact.

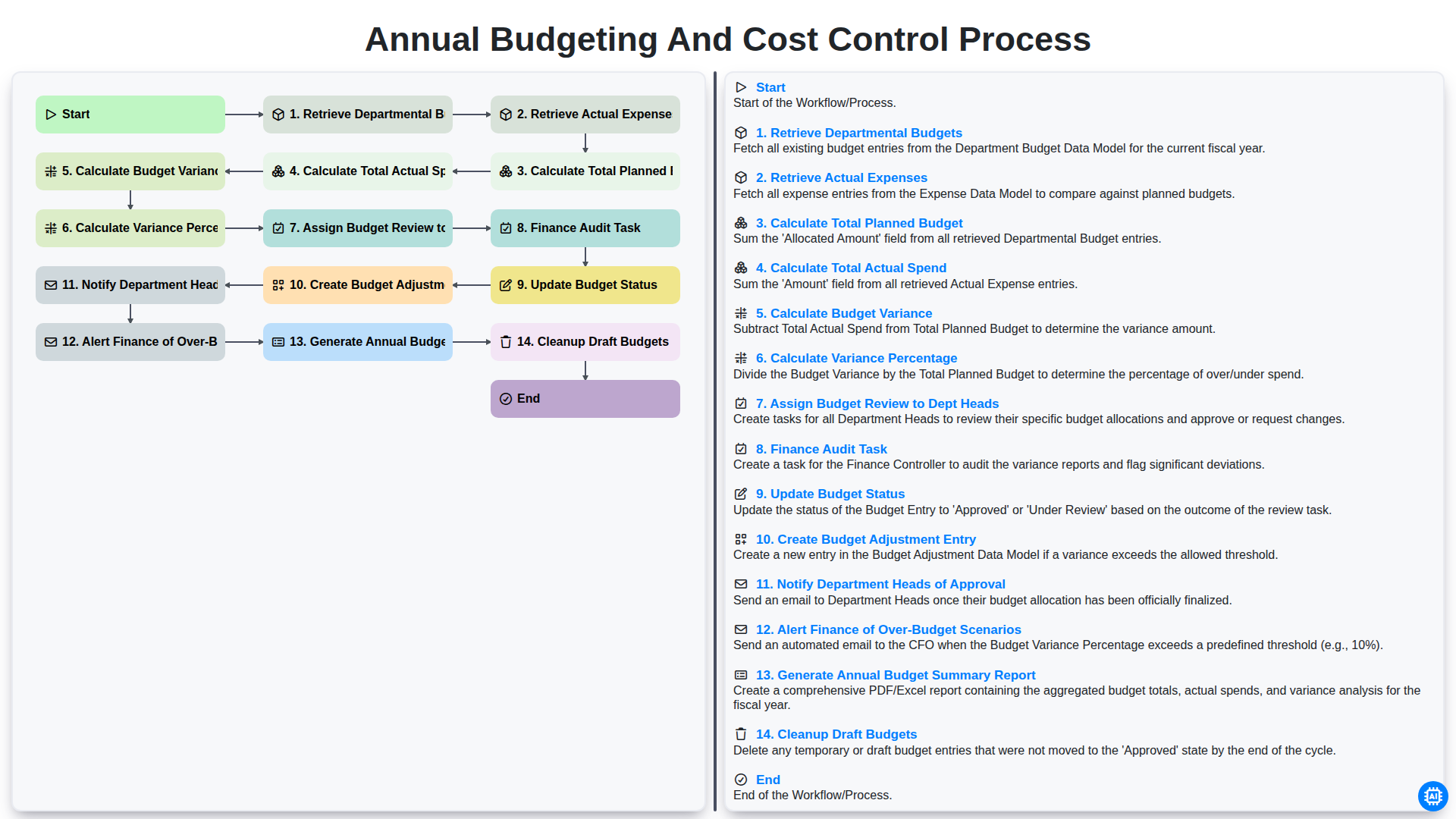

Phase 1: Data Collection and Aggregation

The foundation of a successful annual budget relies on the precision of the data used to build it. The first phase of the workflow, Data Collection and Aggregation, is a critical period focused on gathering all necessary financial inputs to create a comprehensive view of the company's fiscal standing.

This stage begins with two primary data retrieval tasks: Retrieving Departmental Budgets from the previous period and Retrieving Actual Expenses incurred throughout the current fiscal year. By pulling these datasets into a single environment, the finance team can establish a clear baseline for comparison.

Once the raw data is consolidated, the workflow moves into the calculation phase. Here, the system automates the heavy lifting by performing several key computations:

- Calculating the Total Planned Budget: Aggregating all departmental projections to determine the organization's overall intended spend.

- Calculating the Total Actual Spend: Summing all realized costs to understand the true outflow of capital.

- Calculating Budget Variance: Identifying the raw numerical difference between what was planned and what was actually spent.

- Calculating Variance Percentage: Converting those differences into percentages to provide context on the scale of the deviation.

By automating these calculations, the organization eliminates much of the manual error associated with spreadsheets, ensuring that the subsequent phases of review and auditing are built upon a foundation of mathematical integrity.

Retrieving Departmental Budgets and Actual Expenses

The foundation of a successful budgeting cycle lies in the accuracy of your initial data collection. The process begins with the systematic retrieval of two critical datasets: Departmental Budgets and Actual Expenses.

First, the workflow initiates a retrieval of all predefined departmental budgets for the upcoming or current fiscal period. This involves pulling the approved financial targets, allocation limits, and strategic cost projections established during the previous planning phase. This step ensures that the baseline for comparison is clearly defined and officially documented.

Simultaneously, the system must pull the most recent actual expenditure data from your general ledger or accounting software. By retrieving real-time or period-end actual expenses, you eliminate the risk of manual entry errors and ensure that the comparison is based on single source of truth data. This synchronized retrieval is vital; without an accurate snapshot of both what was planned and what has actually been spent, any subsequent variance analysis would be fundamentally flawed.

Phase 2: Quantitative Analysis and Variance Calculation

Once the necessary data has been gathered, the process moves from data collection into the critical analytical stage. This phase is where the raw numbers are transformed into actionable intelligence by identifying the gap between intentions and reality.

The core of this phase involves a systematic series of calculations to determine the health of your fiscal plan. First, the Total Planned Budget is aggregated to establish the baseline for the period, which is then compared against the Total Actual Spend to pinpoint exactly how much capital has been utilized.

The heart of the analysis lies in calculating the Budget Variance-the absolute difference between what was allocated and what was actually spent. However, looking at raw currency figures alone can be misleading, which is why we also calculate the Variance Percentage. This percentage provides vital context, allowing the finance team to understand the scale of the deviation relative to the size of the department's budget. By quantifying these discrepancies, the organization can distinguish between minor fluctuations and significant fiscal drifts that require immediate intervention.

Calculating Total Planned Budget and Actual Spend

To ensure a precise financial overview, the process begins by aggregating the individual departmental budgets to Calculate the Total Planned Budget. This step consolidates all allocated funds across the organization, providing a clear baseline for the entire fiscal year. Once the roadmap is established, the next critical step is to Calculate the Total Actual Spend by summing all real-time expenditures and historical costs incurred during the period. By comparing these two figures side-by-side, the organization gains a high-level view of its financial commitments versus its actual liquidity, serving as the foundation for all subsequent variance analysis and auditing.

Measuring Performance: Budget Variance and Percentage Analysis

Once the raw data for planned budgets and actual expenditures is collected, the true essence of the budgeting process begins: the analytical deep dive. The core of this stage lies in two critical calculations that transform static numbers into actionable intelligence: Budget Variance and Variance Percentage.

Calculating the Budget Variance involves a straightforward but vital subtraction: determining the difference between your Total Planned Budget and your Total Actual Spend. This figure tells you the magnitude of the gap-whether you are operating within your means or facing a deficit. However, a raw dollar amount alone can be misleading; a $5,000 overage is catastrophic for a small department but negligible for an enterprise-wide fund.

To provide necessary context, we must then calculate the Variance Percentage. By dividing the variance by the original planned budget, we arrive at a ratio that standardizes performance across all departments. This percentage allows leadership to identify which specific areas are experiencing disproportionate swings in spending, regardless of their budget size.

By focusing on these two metrics, the finance team can move beyond mere bookkeeping and begin identifying patterns of inefficiency or unexpected cost drivers, setting the stage for more informed decision-making in the next phase of the audit.

Phase 3: Review and Audit Workflow

Once the initial calculations are complete, the process transitions from data processing to critical evaluation. This phase is where the raw numbers are scrutinized to ensure accountability and fiscal accuracy. The workflow follows a structured sequence of verification and oversight:

- Assign Budget Review to Dept Heads: The calculated variances are distributed to the respective department heads. This step empowers leaders to take ownership of their numbers and provide necessary context for any discrepancies.

- Finance Audit Task: To ensure the integrity of the data, the Finance team conducts a rigorous audit. This step verifies that the retrieved expenses and departmental budgets align with company policy and that no manual entry errors have occurred.

- Update Budget Status: Following the audit, each budget line item is updated to reflect its current state-whether it is Under Review, Approved, or Requires Adjustment.

- Create Budget Adjustment Entry: For departments that have exceeded their limits or require reallocation of funds, a formal adjustment entry is created. This ensures that the Plan remains a living, accurate document.

- Notify Department Heads of Approval: Once the audit and any necessary adjustments are finalized, an automated notification is sent to department heads, signaling that their finalized budgets are ready for implementation.

- Alert Finance of Over-Budget Scenarios: As a critical safeguard, the system triggers high-priority alerts to the Finance department whenever a budget variance exceeds a predefined threshold, allowing for immediate intervention and strategic decision-making.

Departmental Reviews and Finance Auditing

Once the initial variance analysis is complete, the workflow shifts from raw data processing to human oversight and accountability. The process begins by assigning budget reviews to Department Heads, requiring them to scrutinize the discrepancies between their planned allocations and actual expenditures. This step is critical for identifying whether variances are due to one-time operational spikes, unforeseen market shifts, or systemic inefficiencies.

Following the departmental review, the process moves into the Finance Audit Task. During this phase, the finance team conducts a rigorous validation of the reported figures, ensuring that all entries are accurate and that the departmental justifications align with company-wide fiscal policies. This audit acts as a safeguard against errors and ensures that any proposed adjustments are grounded in verifiable data.

The final stage of this phase involves updating the official Budget Status within the system. Once the audit is finalized, the workflow triggers the creation of budget adjustment entries for any approved reallocations. To maintain transparency and momentum, the system automatically notifies Department Heads of approvals and simultaneously triggers alerts to the Finance team regarding any over-budget scenarios. This closed-loop communication ensures that leadership is never blindsided by fiscal deviations and that all stakeholders remain aligned with the organization's strategic financial goals.

Phase 4: Finalizing Adjustments and Status Updates

Once the initial review and audit phases are complete, the workflow moves into the critical stage of formalizing the numbers. This phase is where the preliminary calculations transition into official financial records. The process begins with the Finance Audit Task, where the finance team verifies the accuracy of the variance calculations and ensures all departmental justifications are documented.

Following the audit, the workflow triggers a Budget Status Update, officially marking the budget period as Reviewed or Finalized in the system. If significant discrepancies were identified during the review, the team must Create Budget Adjustment Entries to reallocate funds or correct overages.

To ensure transparency and alignment across the organization, the system will automatically Notify Department Heads of Approval for those within their limits, while simultaneously triggering an Alert to Finance for Over-Budget Scenarios that require immediate managerial intervention. Finally, to maintain a clean and efficient financial environment, the process concludes with the Cleanup of Draft Budgets, removing any obsolete or unapproved versions to ensure that only the single source of truth remains in the system.

Managing Budget Adjustments and Approval Notifications

Once the budget variance analysis is complete, the workflow shifts from evaluation to action. This stage begins with the Create Budget Adjustment Entry step, where any necessary reallocations or corrections identified during the audit are formally documented. This ensures that the budget remains a living document that accurately reflects the organization's real-time financial position.

Once adjustments are finalized, the system moves into the communication phase. The workflow automatically triggers a Notify Department Heads of Approval task, ensuring that leaders are immediately aware of their updated financial boundaries. Crucially, to prevent unforeseen deficits, the process also includes an automated Alert Finance of Over-Budget Scenarios. This proactive notification ensures that the finance team can intervene immediately when actual spending exceeds planned allocations, allowing for swift, data-driven decision-making before minor discrepancies turn into significant financial risks.

Proactive Monitoring: Handling Over-Budget Scenarios

One of the most critical features of a robust budgeting workflow is the ability to transition from passive observation to active intervention. In a streamlined process, the system does not simply record a deficit; it triggers an Alert Finance of Over-Budget Scenarios task the moment a variance threshold is breached.

This automated alert acts as an early warning system, ensuring that the Finance team is notified of potential fiscal leaks before they escalate into year-end crises. By integrating real-time alerts into the workflow, organizations can move away from post-mortem accounting and toward proactive management. Instead of discovering a budget overrun during the final audit, leadership can immediately investigate the root cause, evaluate the necessity of a Budget Adjustment Entry, and implement corrective measures-such as reallocating funds or scaling back non-essential expenditures-while there is still time to balance the scales.

Phase 5: Reporting and Process Cleanup

The final stage of the budgeting cycle focuses on transforming raw data into actionable intelligence and ensuring the integrity of your financial records. Once the variances have been analyzed and adjustments have been made, the workflow transitions from calculation to communication and maintenance.

The process begins with the generation of the Annual Budget Summary Report. This document serves as the single source of truth, consolidating the total planned budget, actual spend, and final variances into a high-level overview for stakeholders. This report is critical for identifying long-term fiscal trends and informing the strategic planning for the upcoming fiscal year.

Parallel to reporting, the system triggers automated alerts for over-budget scenarios, ensuring that Finance teams can immediately address significant discrepancies. However, to maintain a clean and efficient financial environment, the process concludes with the cleanup of draft budgets. This step involves archiving incomplete entries and removing any unfinalized budget versions, ensuring that only approved, finalized figures remain in the active ledger. By closing the loop with these administrative checks, you ensure that your budget management system remains organized, accurate, and ready for the next fiscal cycle.

Generating the Annual Budget Summary Report

Once the budget validation process is complete and all variances have been addressed, the final stage of the workflow is the generation of the Annual Budget Summary Report. This report serves as the single source of truth for the organization, consolidating all departmental data into a comprehensive high-level overview.

This document is more than just a collection of numbers; it is a strategic tool used by executive leadership to assess the company's financial health and evaluate the effectiveness of cost-control measures implemented throughout the year. The report provides a clear, side-by-side comparison of planned versus actual expenditures, highlighting which departments operated within their means and which required budgetary adjustments.

By automating this generation, the finance team eliminates the risk of manual entry errors and ensures that stakeholders receive a precise, real-time snapshot of the company's fiscal performance. This summary report becomes the foundational blueprint for the following year's financial planning and long-term strategic decision-making.

Finalizing the Cycle: Cleaning Up Draft Budgets

As the annual budgeting cycle nears its conclusion, the final, often overlooked step is the Cleanup of Draft Budgets. Once all reviews are complete, adjustments are recorded, and approvals are distributed, it is critical to transition from a work-in-progress state to a finalized state within your financial system.

Leaving old drafts or unapproved versions in your accounting software can lead to significant data integrity issues, such as accidental reporting of outdated figures or confusion during mid-year audits. This stage involves archiving all superseded versions and ensuring that only the single, authoritative Master Budget remains active for the upcoming fiscal year. By systematically removing the noise of previous iterations, you ensure that your cost control measures are based on a clean, accurate, and unified financial baseline, providing a solid foundation for the year ahead.

Resources & Links

- Investopedia: Budgeting and Variance Analysis Guide: A deep dive into the fundamental principles of budgeting, variance analysis, and financial forecasting to support the quantitative phase of the workflow.

- AccountingTools: Cost Control Techniques: Comprehensive resources on cost control processes, audit procedures, and managing departmental expenses within a corporate structure.

- Gartner: Financial Planning and Analysis (FP&A) Best Practices: Insights into enterprise-level workflows for budgeting, including automated reporting and managing organizational budget adjustments.

- Forbes Advisor: Managing Business Budgets: Expert advice on overseeing departmental budgets, conducting reviews, and implementing effective financial oversight strategies.

- ProQuest: Financial Audit and Compliance Standards: Resources regarding the importance of the finance audit task and maintaining accuracy during the budget finalization phase.

Found this Article helpful?

Facility Management Solution Demo

Keep your facilities running smoothly! ChecklistGuro streamlines maintenance, inspections, and vendor management. Reduce downtime, optimize efficiency, & improve safety. Manage it all with our Work OS.

Related Articles

Industrial Floor Cleaning & Safety Checklist Template

Display Case Temperature Monitoring Checklist Template

The Ultimate Refrigeration Maintenance Checklist: Keeping Your Food Safe

Escalator & Moving Walkway Inspection Checklist Template

The Ultimate Guest Room Cleaning & Inspection Checklist Template

The Ultimate Security Camera Review Checklist Template

Forklift Inspection & Maintenance Checklist Template

Emergency Generator Load Testing Checklist Template

We can do it Together

Need help with

Checklists?

Have a question? We're here to help. Please submit your inquiry, and we'll respond promptly.