A Step-by-Step Guide to the Insurance Claims Processing Workflow

Published: 06/18/2026 Updated: 06/19/2026

Table of Contents

- Introduction to Efficient Claims Management

- Phase 1: Initial Claim Intake and Verification

- Phase 2: Policy Validation and Financial Assessment

- Phase 3: Investigation Setup and Resource Allocation

- Phase 4: Fieldwork, Evidence Collection, and Site Inspection

- Phase 5: Fraud Detection and Risk Mitigation

- Phase 6: Financial Evaluation and Reserve Management

- Phase 7: Settlement Generation and Claimant Communication

- Phase 8: Final Approval and Claim Closure

- Phase 9: Post-Claim Auditing and Performance Reporting

- Resources & Links

TLDR: Streamline your claims management with this comprehensive guide to our automated Insurance Claims Processing Workflow. Learn how this template automates everything from initial claim retrieval and adjuster assignment to fraud detection and final settlement, ensuring accuracy, reducing manual errors, and accelerating the journey from incident report to payment confirmation.

Introduction to Efficient Claims Management

In the fast-paced world of insurance, the speed and accuracy of claims processing are the true benchmarks of operational excellence. A seamless workflow does more than just ensure financial precision; it serves as the backbone of customer trust and institutional stability. When a claim enters the system, it triggers a complex chain of events-from verifying policyholder details and assessing deductibles to managing intricate investigations and fraud detection.

An inefficient workflow leads to bottlenecked manual tasks, increased human error, and, ultimately, dissatisfied policyholders. Conversely, a streamlined, automated, and highly structured process allows adjusters to focus on critical decision-making rather than repetitive data entry. By mastering the lifecycle of a claim-from the initial retrieval of details to the final settlement notification-insurance providers can reduce operational overhead, mitigate risk, and transform a traditionally stressful touchpoint into a demonstration of reliability and efficiency.

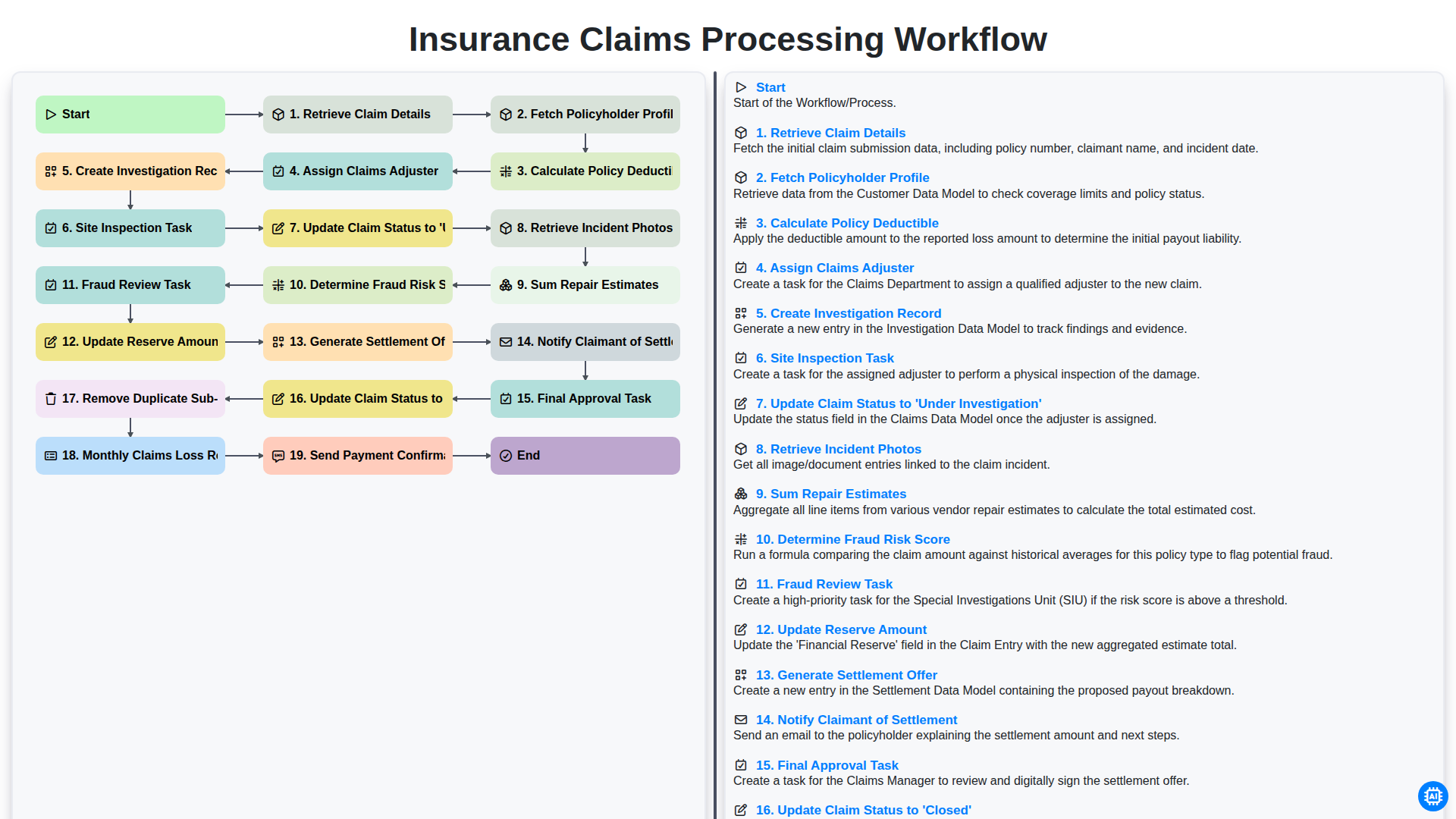

Phase 1: Initial Claim Intake and Verification

The lifecycle of an insurance claim begins with the critical stage of intake and verification, where accuracy is paramount to preventing downstream errors. The process kicks off as soon as a claim is reported, starting with the step to Retrieve Claim Details to establish the core facts of the loss. To ensure the claim is valid, the system must then Fetch Policyholder Profile, verifying that the individual has an active policy and appropriate coverage in place.

Once the policy details are confirmed, the workflow moves into the financial assessment of the policy terms by performing a step to Calculate Policy Deductible, which establishes the baseline amount the claimant is responsible for. With the foundational data verified, the next priority is resource allocation: the system will Assign Claims Adjuster, pairing the case with a professional suited to the specific type of loss. To ensure a formal audit trail is established from the very beginning, the workflow will Create Investigation Record, marking the official start of the claim's internal documentation.

Phase 2: Policy Validation and Financial Assessment

Once the initial claim details have been retrieved, the workflow transitions into a critical stage of verification and financial evaluation. The process begins by fetching the policyholder profile to ensure the coverage is active and valid at the time of the incident. To establish the baseline financial liability, the system must calculate the policy deductible, which determines the portion of the loss the insured is responsible for paying out-of-pocket.

With the fundamental coverage parameters defined, the workflow moves into the assessment phase. The system will assign a claims adjuster to the case and automatically create an investigation record to track all subsequent actions. At this stage, a site inspection task may be triggered to gather physical evidence, and the claim status is officially updated to 'Under Investigation'. This phase ensures that all preliminary data is mathematically sound and that the scope of the investigation is clearly documented before proceeding to deeper scrutiny.

Phase 3: Investigation Setup and Resource Allocation

Once the initial claim details have been retrieved and the policyholder's profile is verified, the process moves into the critical stage of active evaluation. After calculating the applicable policy deductible, the workflow shifts from data collection to resource deployment. The system automatically Assigns a Claims Adjuster to the case and simultaneously Creates an Investigation Record to serve as the single source of truth for the lifecycle of the claim.

To ensure a thorough assessment, a Site Inspection Task is triggered, prompting field personnel to evaluate the physical damage firsthand. During this phase, the claim status is officially updated to 'Under Investigation'. This stage also involves the integration of visual evidence, as the system works to Retrieve Incident Photos submitted by the claimant. By centralizing these tasks, the workflow ensures that the adjuster has all necessary groundwork laid before moving into the complexities of cost estimation and risk assessment.

Phase 4: Fieldwork, Evidence Collection, and Site Inspection

Once the claim has been officially moved to the 'Under Investigation' stage, the process shifts from administrative verification to active field investigation. This phase is critical for establishing the physical reality of the loss and ensuring that the details reported in the initial claim align with the actual damage sustained.

The workflow at this stage focuses on two primary tracks: the gathering of visual evidence and the physical assessment of the incident. First, the system triggers a Site Inspection Task, prompting an adjuster or field representative to visit the location of the loss. During this visit, the objective is to Retrieve Incident Photos and any other relevant physical documentation that captures the scene immediately following the event.

Simultaneously, the adjuster works to bridge the gap between the reported damage and the potential financial liability. This involves gathering all available Repair Estimates from vetted vendors and Summing them to understand the total projected cost of the loss. By consolidating these estimates alongside the photographic evidence, the insurer can build a comprehensive view of the claim's scope. This rigorous collection of data serves as the foundation for the subsequent fraud assessment and the ultimate determination of the settlement amount.

Phase 5: Fraud Detection and Risk Mitigation

Once the initial investigation and repair assessments are underway, the workflow shifts focus to safeguarding the company's assets through rigorous oversight. During this phase, the system automatically executes the Determine Fraud Risk Score step, utilizing data analytics to flag any anomalies in the claim pattern. If a claim exceeds a specific risk threshold, it triggers a mandatory Fraud Review Task, routing the file to a specialized investigative unit for deeper scrutiny. This preventative layer ensures that legitimate claims move forward efficiently while suspicious activities are intercepted before any payouts are issued, maintaining the integrity of the entire claims pool.

Phase 6: Financial Evaluation and Reserve Management

Once the investigation is complete and the repair estimates have been summed, the focus shifts from investigation to the critical financial assessment of the claim. This phase is where the insurer determines the true financial liability by calculating the final indemnity amount. A pivotal step in this stage is the ability to Determine Fraud Risk Score; if a high risk is identified, it triggers a mandatory Fraud Review Task to ensure the integrity of the payout.

If the claim is deemed legitimate, the system must Update Reserve Amount, ensuring that the funds set aside for this specific claim accurately reflect the anticipated payout. This ensures the company's financial stability and accurate provisioning. The process culminates in the Generate Settlement Offer step, where a formal offer is prepared based on the validated costs. Once the offer is presented, the workflow moves to Notify Claimant of Settlement, keeping the policyholder informed and maintaining transparency during the final stages of the claim lifecycle.

Phase 7: Settlement Generation and Claimant Communication

Once the investigation is finalized and the financial obligations are confirmed, the workflow moves into the critical stage of resolution. During this phase, the system automatically performs the Update Reserve Amount step to ensure that the funds set aside for the claim accurately reflect the final calculated costs. Following this, the system will Generate Settlement Offer based on the verified repair estimates and policy terms.

Communication is paramount to maintaining policyholder trust, so the workflow immediately triggers the Notify Claimant of Settlement step, ensuring the customer is informed of the outcome without delay. To conclude the active processing cycle, a Final Approval Task is routed to the necessary supervisors for oversight. Once the final authorization is secured, the system performs the final administrative cleanup by executing the Update Claim Status to 'Closed' step, effectively moving the file out of the active queue and into the archives.

Phase 8: Final Approval and Claim Closure

Once the settlement offer has been accepted and the necessary documentation is in order, the process moves into its final critical stage. The Final Approval Task serves as the ultimate quality control checkpoint, ensuring that the settlement amount aligns with policy terms and that all investigative findings have been properly documented.

After this validation, the workflow proceeds to administrative cleanup and closure. This includes the crucial step to Remove Duplicate Sub-Claims, preventing any overpayment or accounting discrepancies. Once the record is verified, the system will Update Claim Status to 'Closed', officially marking the end of the active lifecycle. To complete the customer experience, a Send Payment Confirmation SMS is automatically triggered, providing the claimant with real-time peace of mind that their funds are on the way. This seamless transition from investigation to payout ensures transparency and maintains trust between the insurer and the policyholder.

Phase 9: Post-Claim Auditing and Performance Reporting

Once a claim reaches its conclusion, the workflow transitions from individual case management to high-level operational oversight. This final phase focuses on long-term data integrity and strategic evaluation through two critical processes: Removing Duplicate Sub-Claims and generating the Monthly Claims Loss Report.

The process begins with a rigorous cleanup of the database to Remove Duplicate Sub-Claims. In complex loss scenarios, multiple entries for the same incident can skew financial data and lead to overpayment risks. By identifying and consolidating these redundancies, the system ensures that the claims ledger remains accurate and auditable.

With a clean dataset established, the workflow culminates in the generation of the Monthly Claims Loss Report. This comprehensive report serves as a vital tool for stakeholders, providing a macro-level view of loss trends, payout frequencies, and total indemnity spent. By analyzing these monthly metrics, insurance providers can identify emerging patterns, adjust underwriting strategies, and ensure the long-term solvency of the fund. This phase transforms individual data points into actionable business intelligence, closing the loop between single incident resolution and enterprise-wide risk management.

Resources & Links

- Insurance Information Institute (III): A primary source for industry statistics, trends, and educational resources regarding insurance claims and policy management.

- American Arbitration Association: Valuable resources for understanding dispute resolution, fraud mitigation, and the legal complexities of claim settlements.

- InsurTech Digital: Insights into how automation and AI are optimizing the claims workflow, from automated intake to digital site inspections.

- Coalition Against Insurance Fraud: Expert resources for understanding fraud risk scoring, detection patterns, and implementing fraud review tasks in the workflow.

- Claims Management Best Practices Guide: Detailed documentation on loss reserve management, financial auditing, and maintaining accurate claims loss reports.

- Workflow Automation & Process Excellence: Technical insights into optimizing end-to-end business processes and managing task assignments within complex enterprise workflows.

Found this Article helpful?

Case Management Solution Demo

Streamline your casework & improve outcomes! ChecklistGuro centralizes case details, tasks, & communication. Enhance efficiency, ensure compliance, & deliver exceptional service. Manage it all with our Work OS.

Related Articles

Streamline Your Deals: The Ultimate Real Estate Case Management Checklist Template

Streamline Your Debt Collection: A Case Management Checklist Template

Cybersecurity Incident Response: Your Checklist Template for Success

Streamline Your Case Management: The Ultimate Checklist Template

Mastering IP: Your Intellectual Property Case Management Checklist Template

HR Case Management Checklist Template: Your Guide to Fair & Compliant Investigations

Streamlining Veteran Care: Your Comprehensive Case Management Checklist Template

Mastering Investigations: Your Case Management Checklist Template Guide

We can do it Together

Need help with

Checklists?

Have a question? We're here to help. Please submit your inquiry, and we'll respond promptly.