The Ultimate Monthly Financial Closing Checklist: A Step-by-Step Guide to a Smooth Month-End Close

Published: 07/12/2026 Updated: 07/13/2026

Table of Contents

- Introduction: Why a Structured Month-End Close is Vital

- Step 1: Bank and Cash Reconciliation

- Step 2: Accounts Payable (AP) Review

- Step 3: Accounts Receivable (AR) Verification

- Step 4: Managing Prepaid Expenses and Accruals

- Step 5: Fixed Asset Management and Depreciation

- Step 6: Inventory and Cost of Goods Sold (COGS) Audit

- Step 7: Intercompany and Sub-ledger Reconciliation

- Step 8: Financial Statement Review & Reporting

- Step 9: Period Closing & Ledger Lockdown

- Best Practices for a Faster Closing Cycle

- Conclusion: Ensuring Accuracy and Compliance

- Resources & Links

TLDR: Master your month-end process with this comprehensive guide and checklist template. Learn how to streamline your financial closing cycle, reduce errors, and ensure accuracy by following a structured, step-by-step approach to reconciling accounts, verifying balances, and finalizing financial statements for a seamless period close.

Introduction: Why a Structured Month-End Close is Vital

For any business, the end of the month is more than just a date on the calendar; it is a critical period of reflection and verification. The month-end closing process is the heartbeat of your financial management, serving as the bridge between raw daily transactions and actionable financial intelligence.

Without a structured closing process, your financial data is merely a collection of numbers prone to errors, omissions, and inconsistencies. A haphazard approach to closing the books can lead to surprises during tax season, inaccurate cash flow projections, and-most dangerously-poorly informed strategic decisions made on the back of flawed data.

A disciplined, repeatable month-end checklist does much more than just ensure accuracy. It provides several key benefits:

- Enhanced Accuracy and Integrity: It ensures that every transaction is accounted for, reducing the risk of fraud, duplicate payments, or missed revenue.

- Improved Decision-Making: Accurate financial statements allow leadership to understand true profitability and liquidity, enabling confident forecasting and budgeting.

- Regulatory Compliance and Audit Readiness: A consistent closing routine creates a clear paper trail, making year-end audits smoother and more cost-effective.

- Operational Efficiency: By defining clear responsibilities and deadlines, you eliminate the month-end crunch, reducing stress on your accounting team and preventing bottlenecks.

By implementing a standardized checklist, you transform your accounting department from a reactive unit into a proactive driver of business growth.

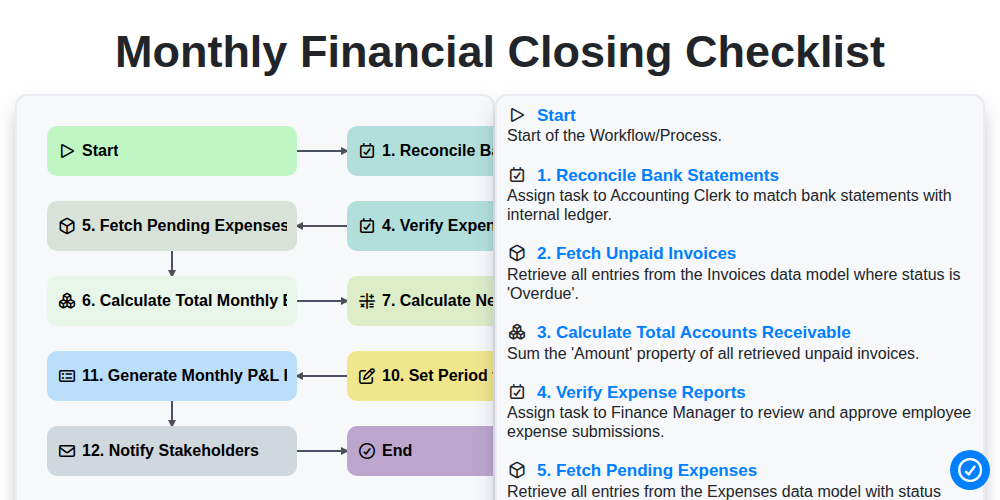

Step 1: Bank and Cash Reconciliation

The foundation of a reliable monthly close begins with ensuring that your records match the actual movement of money. Bank and Cash Reconciliation is the process of comparing your internal cash ledgers against your bank statements to identify any discrepancies.

During this step, you should verify that every transaction-including deposits, withdrawals, bank fees, and interest earned-is accurately recorded in your accounting software. This is also the critical time to hunt for hidden errors, such as uncleared checks, outstanding deposits, or unauthorized transactions. A successful reconciliation ensures that your cash balance is accurate, which prevents downstream errors in budgeting and prevents the much larger headache of discovering a shortage during tax season. Never proceed to the next step of the closing process until your bank balance and your book balance are perfectly synchronized.

Step 2: Accounts Payable (AP) Review

The Accounts Payable (AP) review is a critical step in ensuring that your company's liabilities are accurately recorded and that you have a clear picture of your upcoming cash outflows. An incomplete AP review can lead to overstated profits and unexpected surprises in your cash flow later in the month.

To perform an effective AP review, start by ensuring all vendor invoices received during the period are recorded in the correct accounting period. Check for any unrecorded liabilities-often referred to as unrecorded liabilities-by reviewing invoices that arrived after the month-end but pertain to the previous month.

During this process, you should also:

- Verify Invoice Accuracy: Match purchase orders (POs) with receiving reports and vendor invoices (three-way matching) to prevent overpayment.

- Check for Duplicate Payments: Scan for duplicate invoice numbers or amounts to avoid unnecessary cash leakage.

- Review Aging Reports: Analyze your AP Aging Report to identify overdue balances and prioritize payments to maintain good vendor relationships and avoid late fees.

- Reconcile Vendor Statements: Periodically compare your internal records against statements sent by key suppliers to catch any discrepancies in balances or missing credits.

By diligently reviewing your accounts payable, you ensure that your expenses are fully captured, providing a true representation of your current debt and upcoming financial obligations.

Step 3: Accounts Receivable (AR) Verification

After ensuring your cash levels are reconciled, the next critical step is to verify the accuracy of your Accounts Receivable (AR). This stage is all about ensuring that every dollar owed to your business is properly documented, billed, and accounted for in the correct period.

The primary goal of AR verification is to confirm that your sales revenue matches your outstanding invoices and that your aging report reflects the true state of your collections. During this process, you should perform the following sub-steps:

- Invoice Matching: Cross-reference all invoices issued during the month against your sales orders and shipping documents to ensure no revenue was missed or double-counted.

- Aging Report Review: Examine your AR Aging Report to identify overdue accounts. This helps in assessing the quality of your receivables and determining if any bad debt provisions need to be adjusted.

- Credit Memo Audit: Review all credit memos and returns issued during the period to ensure they are properly authorized and correctly applied against the outstanding balances.

- Unapplied Credits Check: Scrutinize any unapplied payments or unallocated credits. Leaving these floating in your ledger can artificially inflate or deflate your actual receivables.

By meticulously verifying your AR, you prevent revenue leakage and ensure that your balance sheet accurately represents the liquidity available to your company.

Step 4: Managing Prepaid Expenses and Accruals

Accrual accounting is the backbone of an accurate monthly close, as it ensures that revenues and expenses are recorded in the period they actually occur, rather than just when cash changes hands. To maintain the integrity of your financial statements, you must meticulously review your prepaid expenses and accruals.

First, address prepaid expenses by reviewing your prepaid schedule. When you pay for services in advance-such as annual insurance premiums or software subscriptions-the cost shouldn't hit your profit and loss statement all at once. Your task is to calculate the portion of the prepayment that has expired during the month and move it from the balance sheet to the expense account via an adjusting journal entry.

Simultaneously, you must identify and record accruals. This involves capturing expenses that have been incurred during the current month but have not yet been invoiced or paid. Common examples include utilities, employee wages, or unbilled professional services. Without these entries, your monthly expenses will be understated, leading to an inflated view of your profitability. By capturing these liabilities accurately, you ensure a true reflection of your company's financial obligations and a much cleaner transition into the next period.

Step 5: Fixed Asset Management and Depreciation

Ensuring your fixed asset register is accurate is critical for maintaining an accurate balance sheet and calculating correct period expenses. During the monthly close, you must verify that all new acquisitions, disposals, and transfers are properly recorded.

Start by reviewing any new assets purchased during the month to ensure they have been capitalized correctly and assigned the appropriate useful life. Conversely, if any equipment or property was sold or decommissioned, ensure the corresponding gain or loss is recognized and the asset is removed from the books. Finally, perform a check on your depreciation calculations to ensure that the monthly depreciation expense is accurately applied to both the income statement and the accumulated depreciation account. This step prevents discrepancies in your net book value and ensures your long-term asset valuations remain precise.

Step 6: Inventory and Cost of Goods Sold (COGS) Audit

At the heart of every product-based business lies the accuracy of its inventory valuation and the precision of its Cost of Goods Sold (COGS). An error in this step can ripple through your entire income statement, leading to inflated profit margins or unexpected losses.

To ensure your monthly closing is accurate, you must reconcile your physical stock levels with your digital records. This process involves verifying that all received goods have been logged, all shipped goods have been deducted, and any discrepancies-such as shrinkage, damage, or waste-have been properly accounted for.

Furthermore, auditing your COGS requires a deep dive into your unit costs. You must ensure that all direct materials, direct labor, and manufacturing overheads are correctly allocated. A thorough review prevents hidden costs from accumulating and ensures that your gross margin reflects the true economic reality of your operations. By reconciling these figures monthly, you maintain the integrity of your margins and prevent significant year-end adjustments.

Step 7: Intercompany and Sub-ledger Reconciliation

For businesses operating with multiple entities or complex accounting structures, reconciliation at the sub-ledger level is critical to ensuring the integrity of the general ledger. This step involves verifying that the detailed records maintained in subsidiary ledgers-such as the accounts payable, accounts receivable, and fixed asset modules-align perfectly with the summarized totals recorded in the general ledger.

If you are managing multiple subsidiaries, the intercompany reconciliation process becomes even more vital. You must ensure that all-to-all transactions, such as internal transfers, management fees, or shared service charges, are matched and balanced across all involved entities. Discrepancies in intercompany accounts are a common source of phantom profits or losses that can distort the consolidated financial picture. Failing to resolve these mismatches during the monthly close can lead to significant errors in the final consolidated reports and complicate the audit trail.

Step 8: Financial Statement Review & Reporting

Once all the individual account reconciliations and adjustments are complete, the focus shifts from the granular details to the big picture. The financial statement review is the most critical step in the closing process, as it serves as the final quality control mechanism before the data is finalized.

During this phase, you are not just looking at numbers, but looking for meaning within them. The goal is to ensure that the Balance Sheet, Income Statement, and Cash Flow Statement are accurate, complete, and logically consistent.

To perform an effective review, focus on these three core areas:

- Trend and Variance Analysis: Compare the current month's figures against the prior month and the budgeted expectations. Significant fluctuations (variances) should be investigated. If utility costs have doubled or revenue has plummeted, you need to identify the specific transaction or error causing the anomaly.

- Analytical Consistency Check: Ensure that the numbers tell the same story across different reports. For example, if your revenue increased significantly, your Cost of Goods Sold (COGS) should generally reflect a proportional change. If they don't, there may be an unrecorded expense or an error in inventory valuation.

- Final Error Detection: Scrutinize the Income Statement for any glaring omissions, such as missing recurring monthly expenses, and scan the Balance Sheet for unusual balances (such as negative asset accounts or unexpected credit balances in accounts receivable).

This stage is your last opportunity to catch errors before they become part of your permanent financial history. A thorough review ensures that the reports you present to stakeholders, management, or tax authorities are a true and fair representation of your company's financial health.

Step 9: Period Closing & Ledger Lockdown

Once all reconciliations are complete and all entries are verified, it is time for the final and most critical phase: the lockdown. This stage is about more than just finishing tasks; it is about preserving the integrity of your financial data. Period closing involves making the formal decision to close the books, which prevents any further modifications, deletions, or accidental entries into the period you have just finalized.

To execute a proper lockdown, follow these essential sub-steps:

- Post All Final Adjustments: Ensure that all journal entries, including those related to accruals and depreciation, have been fully posted to the General Ledger.

- Verify Sub-ledger Closure: Confirm that all auxiliary modules-such as Accounts Payable, Accounts Receivable, and Inventory-are fully synchronized with the General Ledger and that no pending transactions remain in these sub-modules.

- Run Final Trial Balance: Perform a final check of the Trial Balance to ensure that debits and credits are in balance and that no unexpected discrepancies have emerged during the final posting.

- Restrict Access/Lock the Period: Use your accounting software's administrative controls to lock the specific period. This prevents users from back-dating transactions, which is vital for maintaining a clean audit trail and ensuring that your reported numbers remain consistent.

By strictly enforcing a ledger lockdown, you create a point in time snapshot that serves as the single source of truth for your financial reports, ensuring that the data used for decision-making is stable and tamper-proof.

Best Practices for a Faster Closing Cycle

Achieving a faster month-end close is not just about working harder; it is about working smarter through standardization and proactive management. To reduce the time spent in the closing window and minimize errors, consider implementing these industry best practices:

- Adopt a Continuous Close Mindset: Don't wait until the last day of the month to start your reconciliations. Perform bank reconciliations and review Accounts Payable regularly throughout the month. The more you clear during the period, the less bottleneck you create during the final week.

- Standardize and Automate: Manual data entry is the enemy of speed. Leverage automation for repetitive tasks like intercompany reconciliations and depreciation calculations. Use standardized templates for accruals and prepaid expense tracking to ensure consistency across every period.

- Establish a Clear Closing Calendar: Create a centralized timeline that assigns specific deadlines and owners to every step of the checklist. When every team member knows exactly when the AP review must end and the ledger lockdown must begin, it eliminates ambiguity and prevents downstream delays.

- Prioritize Materiality: Focus your deepest scrutiny on high-value accounts. While accuracy is vital, applying the same level of granular detail to every minor petty cash entry as you do to your primary inventory valuation can lead to unnecessary delays.

- Perform Post-Close Reviews: Once the period is closed, conduct a brief post-mortem. Identify which steps caused delays or where discrepancies were found. Use these insights to refine your checklist and address the root causes of bottlenecks for the following month.

Conclusion: Ensuring Accuracy and Compliance

Implementing a structured monthly closing checklist is more than just an administrative necessity; it is a fundamental pillar of financial integrity. By systematically working through bank reconciliations, accruals, and ledger lockdowns, you transform the month-end process from a frantic scramble into a predictable, streamlined routine. This disciplined approach does more than just ensure that your numbers are accurate-it mitigates the risk of fraud, identifies costly errors before they escalate, and provides the high-quality data required for strategic decision-making.

Ultimately, a rigorous closing process fosters transparency and builds trust with stakeholders, auditors, and regulatory bodies. While the checklist requires diligence and consistency, the long-term rewards of improved compliance, reduced closing cycles, and a single source of truth for your company's financial health are invaluable. Embrace these steps as a roadmap to financial excellence and use them to drive your organization toward sustainable growth.

Resources & Links

- Investopedia : A comprehensive resource for understanding fundamental accounting principles, financial terms, and the mechanics of the closing process.

- Accounting Today : Industry news and professional insights for accountants regarding best practices in financial reporting and period-end procedures.

- AICPA : The official site for professional standards and compliance guidelines essential for maintaining accuracy during the ledger lockdown.

- NetSuite : Practical insights and tools for automating complex tasks like intercompany reconciliations and inventory management.

- Forbes Advisor : Business-centric perspectives on managing cash flow, accounts payable, and the importance of financial oversight for company growth.

- Accounting Software Solutions : Resources on using automation to streamline bank reconciliations and reduce manual errors in the monthly closing cycle.

Found this Article helpful?

Accounting Management Solution Demo

Move beyond rigid, one-size-fits-all software. Leverage a fully programmable accounting environment designed to adapt to your unique workflows, complex hierarchies, and evolving business logic.

Related Articles

The Ultimate Financial Data Integrity Audit Checklist: A Step-by-Step Template for Precision and Compliance

The Ultimate Financial Statement Review Checklist: A Step-by-Step Guide to Ensuring Accuracy and Compliance

Mastering Financial Control: The Ultimate Departmental Budget Monitoring Checklist

The Ultimate Accounts Receivable Collections Checklist: A Step-by-Step Guide to Streamlining Your Cash Flow

The Ultimate Payroll Processing & Compliance Checklist: A Step-by-Step Guide to Error-Free Payroll

The Ultimate Year-End Audit Preparation Checklist: A Step-by-Step Guide to a Stress-Free Audit

The Ultimate Software Implementation Checklist for Accounting Teams: A Step-by-Step Guide to a Seamless Transition

The Ultimate Inventory Valuation & Audit Checklist: A Step-by-Step Guide to Accuracy and Compliance

We can do it Together

Need help with

Accounting Management?

Have a question? We're here to help. Please submit your inquiry, and we'll respond promptly.